As world leaders, policymakers, scientists and activists convene in Dubai for the 28th Conference of the Parties to the United Nations Framework Convention on Climate Change (COP28), one of the many topics of discussion is the role of mandatory disclosure in driving climate change mitigation.

In what has arguably been a watershed year for corporate climate disclosure regulations – including the finalization of the European Union's Corporate Sustainability Reporting Directive (CSRD) and passage of the landmark California Climate Accountability Package (SB-253 and SB-261) – one piece of regulation is noticeably still pending: the U.S. Securities and Exchange Commission’s (SEC) proposed rule to enhance climate-related disclosures for investors. Initially anticipated to become final in 2022, the SEC has delayed a decision on the final rule multiple times, citing the extended review due to thousands of comment letters received from both supporters and opponents.

Concerns Over Scope 3

Much of the opposition to the proposed rule centers on the inclusion of disclosure requirements for Scope 3 greenhouse gas (GHG) emissions, which are indirect emissions generated in a company’s value chain, both upstream (e.g., generated by suppliers) and downstream (e.g., generated by product end-users). While the Scope 3 requirement as currently written would only apply to select companies (see details below), opponents cite two main arguments against the inclusion:

1. Measurement and Reporting Burden: Companies with large, complex value chains would need to collect and aggregate data from numerous sources. Further, this could indirectly impose GHG emissions measurement requirements on privately held companies that would not otherwise be subject to the rule, but that sit within a qualifying public company’s value chain.

2. Data Integrity: Given the breadth of company value chains, Scope 3 reporting largely relies on estimation – including the use of industry average data, proxy data, and other generic data – that some argue limits the integrity of the information companies would be able to report. As a counter to this argument, proponents of Scope 3 point out that estimation also plays a significant role in how traditional financial data are calculated in company annual reporting.

Global Climate Disclosure – With or Without the SEC

Despite sustained pushback to the SEC proposed climate rule, many U.S. companies already track and disclose climate-related performance. According to International Energy Agency (IEA), as of October 2022, 56% of S&P 500 companies were voluntarily disclosing Scope 1 emissions, 55% were disclosing Scope 2 emissions and 38% were disclosing Scope 3 emissions. This is due both to continued investor requests for climate-related information and new reporting laws and regulations passed in the European Union (EU), the state of California, and a growing number of additional jurisdictions globally.

In the time the SEC has spent reviewing reactions to its proposed climate disclosure rule, regulators and lawmakers domestically and abroad have established climate-related disclosure requirements that will apply to many U.S. companies and, in some cases, go beyond the anticipated SEC climate disclosure rule. This is the case with CSRD and the EU’s accompanying European Sustainability Reporting Standards (ESRS), the International Sustainability Standards Board's (ISSB) IFRS Standard and California SB-253 and SB-261. In fact, SEC Chairman Gary Gensler recently stated the California bills could change the baseline for the anticipated SEC climate rule, potentially reducing the cost burden on corporate issuers that are also reporting relevant climate-related disclosures to the state of California.

For Corporate Issuers, Preparation is Key

With certain climate-related disclosure laws and regulations requiring reporting as soon as 2025 for the prior fiscal year, companies should not delay their preparations for compliance. For U.S. companies that have already started reporting climate risk management strategies and associated data in annual ESG reports, many of these required climate-related disclosures will simply make mandatory what is already happening voluntarily.

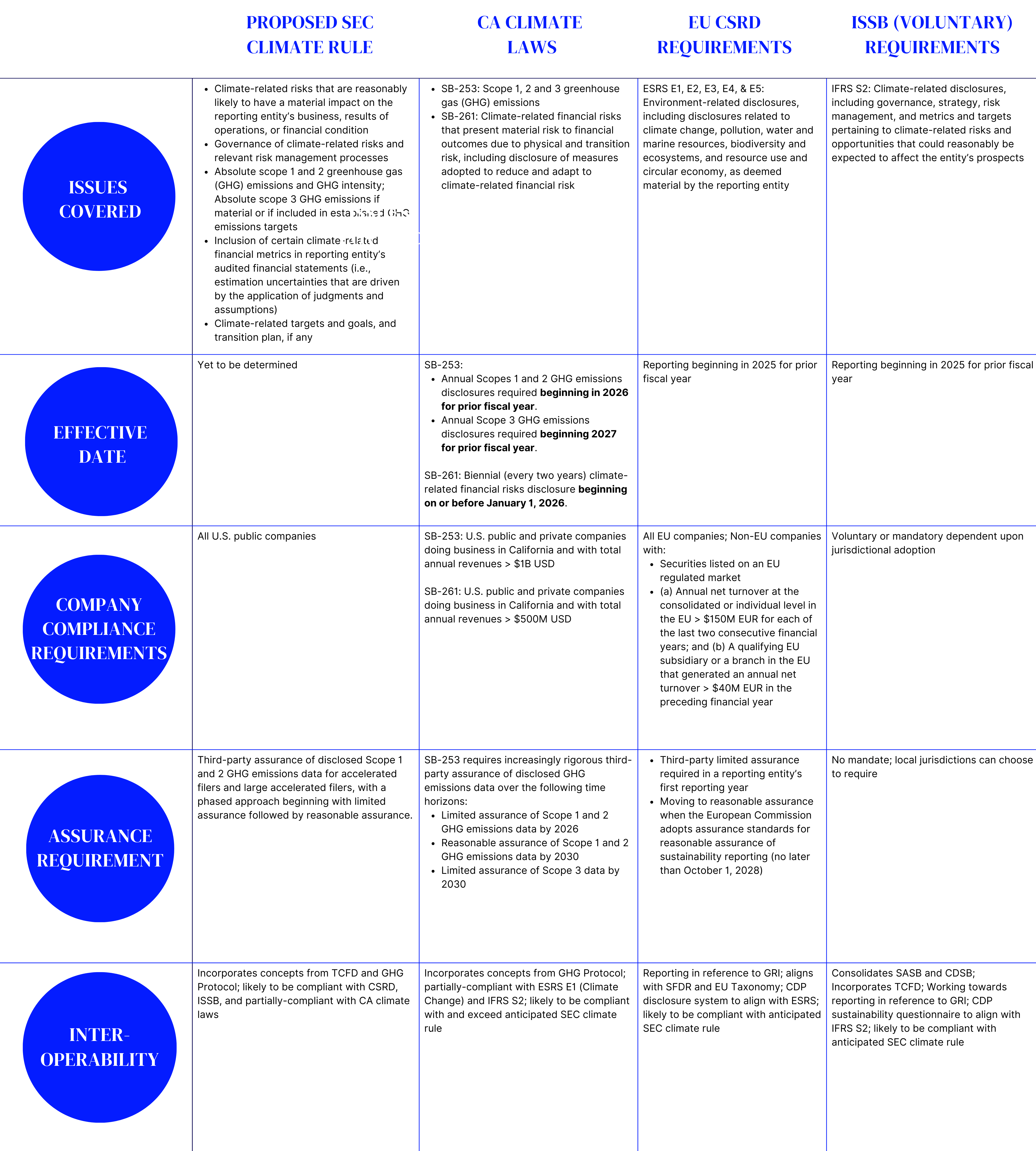

That said, gaps may exist between what companies currently report and what regulations will require, so issuers should review their existing data collection and disclosure practices to identify deltas and develop a strategy to fill those gaps in time for compliance. (See our summary of the latest climate-related disclosure laws and regulations below to understand the disclosure requirements of each and their interoperability with existing standards and laws.)

Future Implications For Annual Reporting

Wide-scale integration of climate-related disclosures in annual financial filings or Forms 10-K within the U.S. is not expected in the near-term beyond what will ultimately be required by the final SEC climate rule. That said, heightened attention and wider adoption of climate-related disclosures could lend a growing number of companies to begin including select climate and other ESG -related disclosures in annual reports and filings, providing a streamlined avenue for investors and other key stakeholders to find decision-useful information within one resource.

It's also important for companies to think beyond quantitative disclosures and work to develop a qualitative narrative to complement the data and provide important context into climate-related strategy and management practices. Much like in financial disclosures, stakeholders value discussion and analysis to understand the broader performance landscape. Companies should invest in crafting an accompanying narrative that addresses climate-related risks and performance for inclusion in their annual filings.

Mathilde Sellars, senior account supervisor, ESG Advisory, (mathilde.sellars@edelmansmithfield.com) and Nina Wilson, senior vice president, ESG Advisory (nina.wilson@edelmansmithfield.com)

Global Climate-Related Disclosure Requirements - Click to view and download